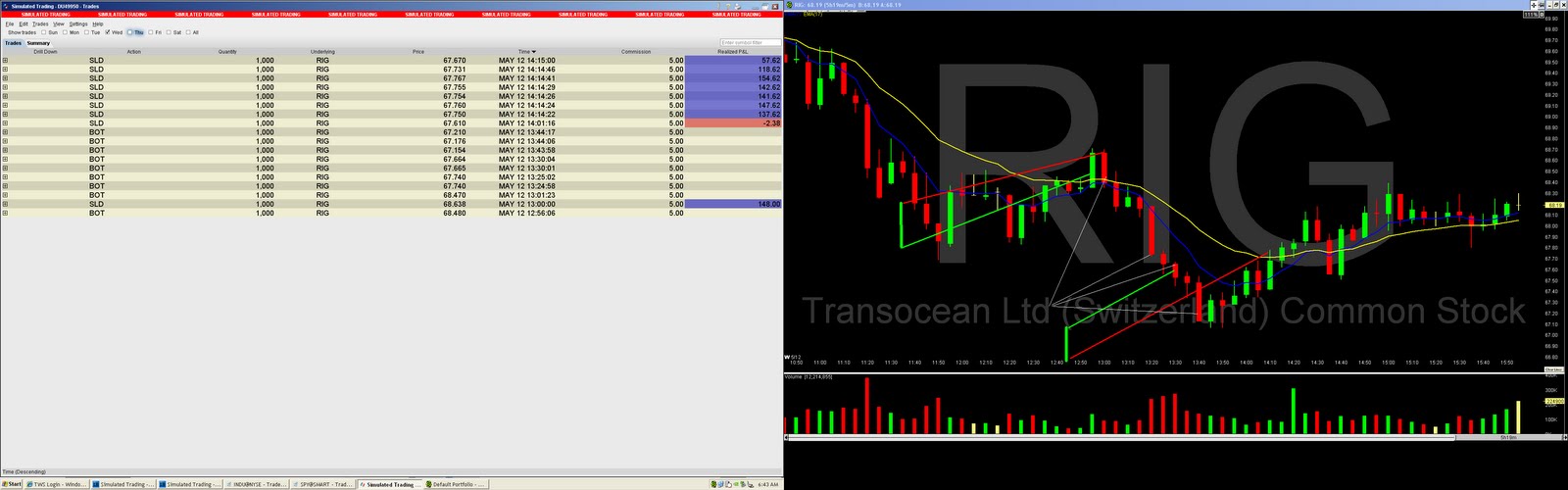

I spent most of the day out of the office but had a chance to look at the markets in the later afternoon. Because of Scott Farnham's attention to the VXX of late, I called it up and thought I'd have a look at the chart. I liked the chart immediately... my forst impression was of how "clean" it looked. But, upon entering, I found it to be rather squirrely. Maybe it was just that it was EOD and the intra-candle volatility was increased.

In any event, my first trade was a scalp for short money paper-gain. My second paper trade was completely against grain, that's woodworker speak for going against the flow. (poor choice #1). For some reason, my first impulse is to look for reversals. Occasionally I ignore this impulse but for some reason, it is how I am wired. Too bad, because this as well as my initial entries over the past few days would have been nice winners had I gone "with the grain," in the direction of momentum. I held the trade (poor choice#2) as I have the past few days and found a good area to really hit hard to bring average price down. Then, as I have done recently, I sold the pop for a modest gain. It was around this time that I found the price really twitchy. Looks like a lot of traders were uncertain and it translated into short-term volatility.

What did I learn today?

1. I have to make my first thought to "go with momo" instead of counter to it. Doing so would have given me very nice gains on each of the past few days. My pattern of being "early" on reversals continues. Which is to say, a pattern of being "wrong" initially.

2. I must sell those losing trades. One of my weak spots is recognizing when I am wrong versus when I am caught in consolidation and need to hold onto my trade idea.

3. Be patient. Await my familiar signs of direction change in order to increase my probablity of a timely entry. After all, if I haven't seen such a sign, why should I play for a reversal of the current momo? Go with the flow instead.